Pay4Bit Review: Why We Added Pay4Bit.net to Our Avoid List (2026)

Pay4Bit cites the FCA in its AML policy but is not on the FCA Register. Two entity names, two virtual offices, a year-old domain, and merchants reporting withheld funds. Full investigation.

⚠ Avoid List — TL;DR

- Pay4Bit references the FCA in its AML policy but does not appear on the FCA Register

- Operates under two different company names in two different countries — both at virtual office addresses

- Domain pay4bit.net is barely a year old (registered January 2025)

- Multiple merchants report withheld funds, impossible verification loops, and threats to refund their customers

- We recommend merchants use NOWPayments, CoinGate, or BTCPay Server instead

We spent time investigating Pay4Bit after seeing multiple merchants reporting the same issues. What we found was concerning enough that we're adding Pay4Bit to our avoid list and publishing a detailed post so other merchants don't get caught.

What Is Pay4Bit?

Pay4Bit (pay4bit.net) is a payment gateway that lets merchants accept credit cards (Visa, Mastercard, Amex) and cryptocurrencies (BTC, USDT, LTC, XRP, SOL). They market themselves as a fast, no-code setup — "accept payments in 3 minutes" — and target SaaS companies, digital product sellers, ecommerce merchants, and freelancers.

It sounds great on paper. But once you look at who is actually behind it, things fall apart fast.

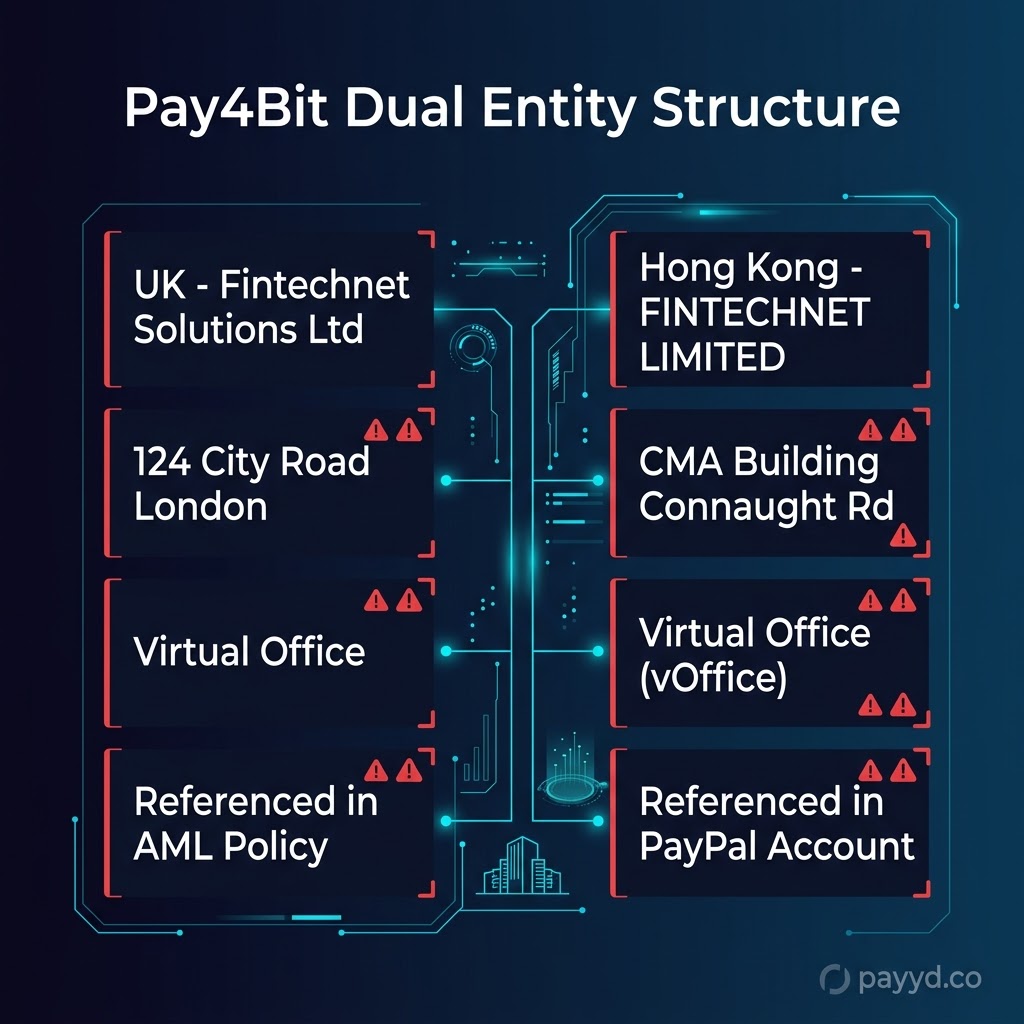

The UK Entity: A London Virtual Office

Pay4Bit's AML policy (published at docs.pay4bit.net) states the service is operated by Fintechnet Solutions Ltd, registered at 124 City Road, London, UK, EC1V 2NX.

The policy name-drops some serious legislation:

- UK Financial Conduct Authority (FCA)

- Proceeds of Crime Act 2002 (POCA)

- UK Criminal Finances Act 2017

- Financial Action Task Force (FATF) recommendations

Impressive. Until you Google the address.

124 City Road, London, EC1V 2NX is one of the most notorious virtual office addresses in the UK. Over 5,400 companies are registered there. It's a mail-forwarding service you can rent for a few pounds a month. There is no Pay4Bit office at that address. There are no Pay4Bit employees. It's a mailbox.

The Hong Kong Entity: Another Virtual Office

Here's where it gets interesting. Pay4Bit's PayPal account is not registered to "Fintechnet Solutions Ltd" in London. It's registered to FINTECHNET LIMITED — a different entity name — at 64-66 Connaught Road Central, CMA Building, Central, Hong Kong, with contact number +852 90429734.

The CMA Building is home to vOffice, a virtual office provider. You can get a registered company address there for about HK$68/month — roughly €8.

So we have:

| UK | Hong Kong | |

|---|---|---|

| Entity name | Fintechnet Solutions Ltd | FINTECHNET LIMITED |

| Address | 124 City Road, London | CMA Building, 64-66 Connaught Rd Central |

| Type of address | Virtual office (5,400+ companies) | Virtual office (vOffice) |

| Referenced in | AML policy, documentation | PayPal account |

Two different company names. Two different countries. Two virtual offices. Zero verifiable physical presence anywhere.

Not on the FCA Register

This is the big one.

Pay4Bit's AML policy explicitly references the FCA, the Proceeds of Crime Act 2002, and the Criminal Finances Act 2017. Reading their documentation, you'd reasonably assume this is a UK-regulated financial services company.

So we checked the FCA Register — the public database where every firm authorised by the FCA to conduct regulated financial activities in the UK is listed.

Neither "Fintechnet Solutions Ltd" nor "Fintechnet Limited" appears on the FCA Register.

For context, every legitimate UK payment processor is immediately findable on the register. Stripe, PayPal, Wise, Revolut — all have FCA registration numbers you can verify in seconds. Pay4Bit does not.

This matters because under the Financial Services and Markets Act 2000, operating a regulated payment service in the UK without FCA authorisation is a criminal offence.

A company that references the FCA in its own compliance documentation but is not actually on the FCA Register is either:

- Misrepresenting its regulatory status to merchants

- Operating without proper authorisation

- Both

Any merchant can verify this themselves at register.fca.org.uk.

The Verification Loop

The pattern we've seen reported by multiple merchants looks like this:

- You sign up, integrate, and start accepting payments. Everything works fine at first.

- After you accumulate a meaningful balance, your account gets flagged for "verification."

- You're asked to provide identity documents — passport, tax ID, selfie with passport.

- You submit everything.

- They ask for the same documents in a different format (e.g., "please send it as a PDF").

- You comply.

- They ask for additional documents — bank statement with your name, address, and IBAN.

- You comply.

- They ask for your passport again. The previous one "could not be verified by our system."

- You submit it again. They decline.

- They threaten to refund your customers if you can't complete verification.

Multiple merchants. Same cycle. Same language in support responses. Same outcome: funds withheld.

The Refund Threat

This is the most alarming tactic. When merchants push back, Pay4Bit threatens to return earned funds to the original customers.

Think about what this means in practice: your customers received your product or service. Pay4Bit collected the payment. But instead of paying you out, they threaten to give the money back to customers who already got what they paid for. The merchant loses both the product and the revenue.

A legitimate payment processor does not weaponise customer refunds as leverage against its own merchants.

The Fee Trap

Even setting aside the withdrawal issues, Pay4Bit's dispute fee structure is punitive:

- €25 charged just for opening a dispute — regardless of outcome

- Additional €40 if the merchant loses the dispute

- €65 total plus the refund amount on a single chargeback

- Transaction fees are already above industry average

Compare this to Stripe (~$15 per dispute) or PayPal (~$20). Pay4Bit charges 3-4x more per dispute than established processors.

The Bigger Picture

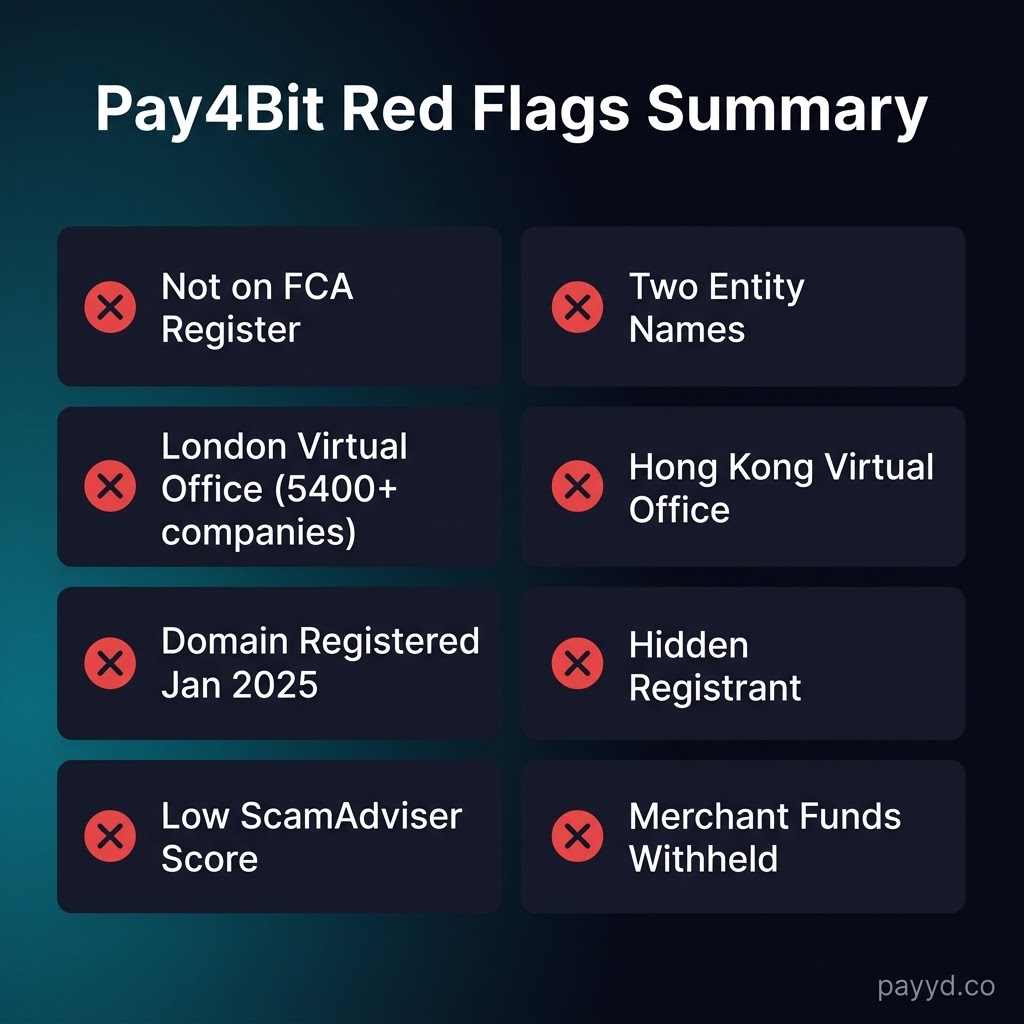

Putting it all together:

- ❌ Not on the FCA Register — despite referencing the FCA in its own AML policy

- ❌ Two different company names across two jurisdictions

- ❌ Virtual office in London (5,400+ companies at the same address)

- ❌ Virtual office in Hong Kong (vOffice provider)

- ❌ No verifiable physical presence anywhere

- ❌ Domain registered January 2025

- ❌ Hidden domain registrant

- ❌ Very low ScamAdviser trust score

- ❌ Multiple independent merchants reporting withheld funds

- ❌ Impossible verification loops (requesting documents that don't exist)

- ❌ Threats to refund customers as leverage

- ❌ Punitive dispute fees (€65 per chargeback)

- ❌ Interrogation of merchant location and travel arrangements

Not a single green flag in that list.

What To Do If You're Affected

If Pay4Bit is currently withholding your funds:

- Screenshot and save everything — all conversations, transaction records, and document submissions before they can delete or modify anything.

- File a report with PayPal — their account is FINTECHNET LIMITED in Hong Kong. PayPal takes misrepresentation seriously.

- Report to Action Fraud UK at actionfraud.police.uk — the UK's national fraud reporting centre.

- Report directly to the FCA — if they reference the FCA but don't appear on the register, the FCA needs to know. This is potentially an unauthorised firm.

- File with the European Consumer Centre in your country for cross-border dispute assistance.

- Leave a factual review on Trustpilot to warn other merchants.

Don't submit any more documents. If you've already provided a passport, tax documents, and bank statements, you've provided more than enough. Further submissions just reset the clock.

Use These Gateways Instead

If you need to accept crypto payments, use a processor with a verifiable legal entity, published leadership, and a track record. Our recommended alternatives:

- NOWPayments — 300+ coins, 0.5% fee, established since 2019

- CoinGate — EU-regulated, fiat settlement, 1% fee

- BTCPay Server — self-hosted, zero fees, non-custodial (you control the keys)

- Our full no-KYC gateway comparison

If a payment processor has no real office, operates under two names in two countries, has existed for barely a year, references the FCA but doesn't appear on the FCA Register, and multiple merchants independently report the exact same pattern of withheld funds — you don't need a lawyer to tell you something is wrong.

Do your due diligence. Check the registers. Read the reviews. And if something feels off, trust your instincts.

FAQ

Is Pay4Bit a scam?

We can't make a legal determination, but the pattern is consistent with known payment-processor scams: virtual offices, misrepresented regulatory status, verification loops after balances accumulate, and refund threats. Multiple independent merchant reports describe the same cycle. We've added Pay4Bit to our avoid list.

How do I check the FCA Register myself?

Go to register.fca.org.uk and search for the firm name. Legitimate UK payment processors appear with an FRN (Firm Reference Number) and a permissions list. "Fintechnet Solutions Ltd" and "Fintechnet Limited" return no results.

What's a safer alternative?

For most merchants: NOWPayments (300+ coins, established) or CoinGate (EU-regulated, fiat settlement). For maximum control and zero gateway risk: BTCPay Server (self-hosted, non-custodial).